18 October 2022 | Climate Tech

Solar is eating the world

By

Marc Andreessen, head of the venture capital firm Andreessen Horowitz, coined the phrase ‘software is eating the world’ in a seminal essay a decade ago to describe just how dominant software companies have become.

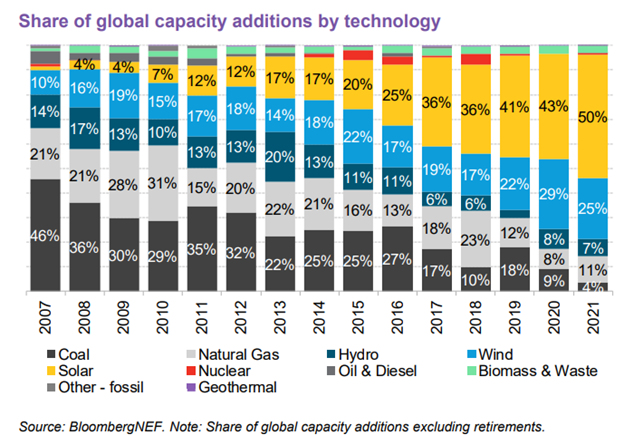

10+ years on, the phrase could now be adapted to ‘solar is eating the world.’ The world is installing more solar capacity than any other form of energy:

Renewable energy, specifically solar, hydro, and wind, represented more than 80% of global capacity additions in 2021. Fossil fuels comprise another ~15%. And even as we’ve discussed growing signs of greenshoots for nuclear energy this year, it barely registered in 2021. 2022 may look a bit different, as new reactors have come online this year.

Back to the solar story. You can see a similar dynamic in terms of planned capacity additions in the U.S., where solar dominates other forms of energy as well. While things like grid interconnection requests include planned projects that won’t all come to fruition (projects fall through for all kinds of reasons), the relative magnitudes of planned projects still illustrate developer preferences.

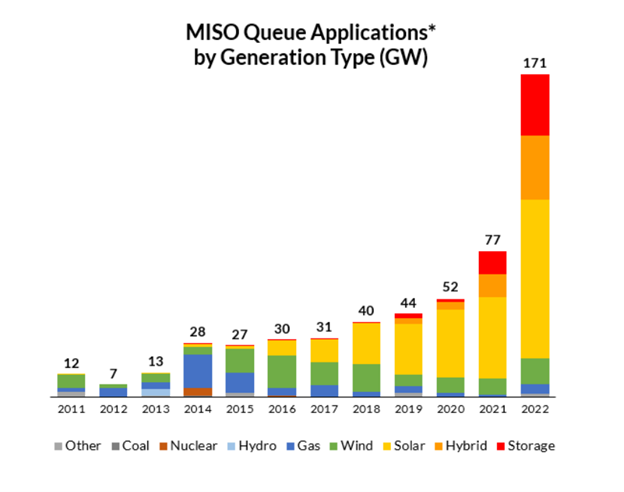

Here’s the picture for MISO, which manages energy generation and high-voltage transmission for 15 states and Manitoba:

Between solar, energy storage, and hybrid projects (frequently solar + energy storage), other forms of planned capacity additions hardly register.

Elsewhere in the world, global energy leaders are unleashing the sun’s power even as some governments make moronic new rules about where solar farms can and can’t be installed (coughs at the U.K.). The Inflation Reduction Act in the U.S. unlocked lots of capital and incentives for renewable energy developers, while China has already doubled solar installations year-over-year in 2022. The International Energy Agency expects solar’s share of capacity additions to continue growing in 2022 and 2023, outpacing other renewables like wind and hydropower.

Why am I reading this now?

Solar and wind power have both come down the cost curve precipitously in recent years. Said differently, it’s gotten much cheaper to harness the free renewable energy they offer, and by many measures, they’re cheaper than all other potential fuel sources. That said, of the two, developing new wind energy projects requires higher capital expenditures in general. Wind turbines are giant, whereas solar panels are more modular, flexible, and easier to deploy.

That helps explain why solar capacity additions are pulling ahead even of wind power this year. Interest rates are rising globally; financing big new wind projects isn’t as easy as it was two years ago. Solar farms are also a bit easier to site – not every place in the world has strong winds, but most get some solid sunshine, at least some of the year.

Lest we forget, hydropower is also a very relevant form of renewable energy. There’s actually more installed hydropower capacity globally than solar – it had a hundred-year head start. But hydropower is even more capital-intensive than building wind farms and can be more disruptive to the surrounding environment than wind or solar farms.

A long way to go

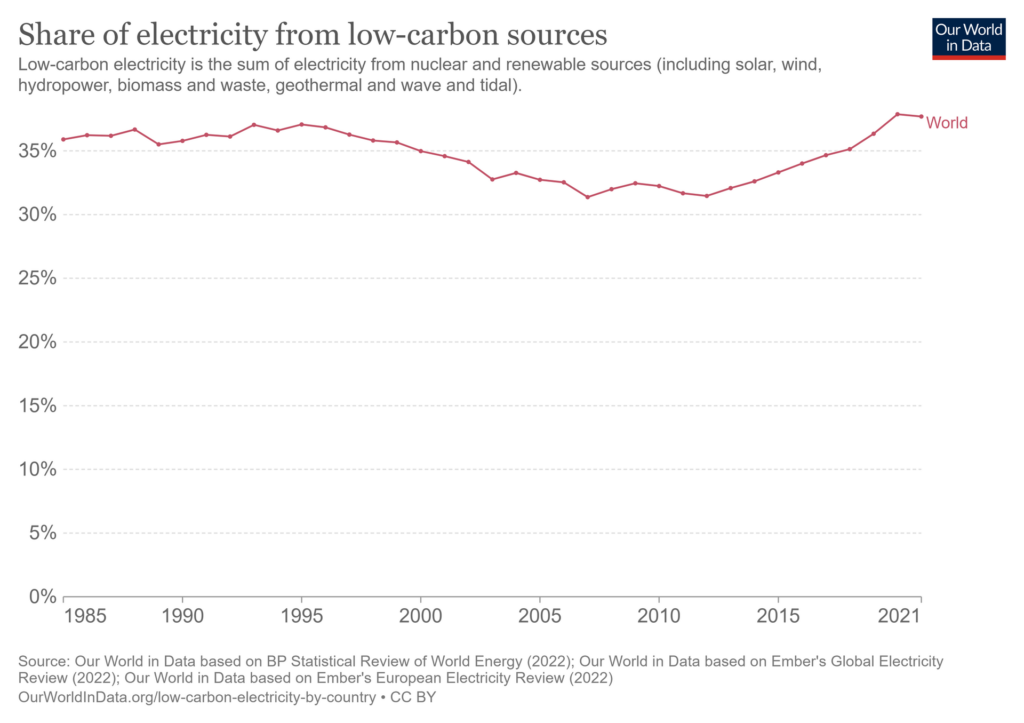

As much progress as solar is making, there’s a long way to go. Low-carbon energy sources, including renewable and nuclear energy (technically non-renewable), provide ~37% of the world’s electricity.

But that percentage share has been pretty stable for decades. Part of the reason for this is that nuclear capacity additions have stalled out. Plus, even as wind and solar have taken off, the denominator (total energy capacity) has grown a lot, too, as fossil fuel-fired capacity – coal in the late 1900s and natural gas since the turn of the century – has expanded significantly.

In short, low-carbon sources more or less have only ‘kept up’ with fossil fuel additions over the last four decades.

Further, low-carbon sources also only provide ~17% of the world’s primary energy. The distinction between this number and the earlier 37% figure is an important one. Electricity is just one form of energy; thermal energy (heat) for industry is critical, too, as is mechanical energy (moving things around). Those types of energy continue to be dominated by fossil fuels, even as renewables make inroads in electricity. To this end, renewables can only go so far without additional technological help. There are some solar-powered car companies, and sails in ships work quite well, but most often, to turn less-energy-dense renewables into high heat for industry or into motion for transport, you need something like batteries to store and condense energy.

Good news: There are plenty of firms working on this challenge. Rondo Energy is one example – they make a battery that turns renewable energy into storable industrial heat and power.

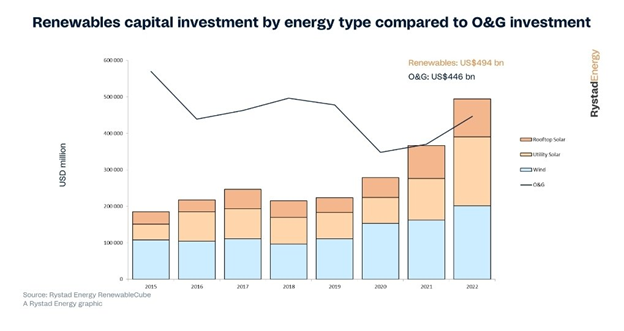

Finally, it’s worth noting that there are positive signs that the momentum for solar (and wind) will be sustained. In 2022, global capital expenditures on solar and wind will exceed those for upstream oil and gas infrastructure for the first time.

The net-net

Many people argue about the merits of different fuel sources, whether fossil, nuclear fission, or renewable. But global capacity additions paint a clear picture, both looking at observed additions from recent years and planned additions for coming ones.

While a lot of factors drive this, including some – like tax subsidies – that are independent of the technology itself, little detracts from the fact that solar looks like a runaway freight train right now. Argue about subsidies and regulations all you want, but most of the world shows a strong preference for solar power.

It’s easy to get caught up in the noise of things like the energy crisis in Europe and to miss the forest for the trees as a result: expanding global solar capacity will make electricity cheaper and reduce global emissions. Still, a lot more will need to go into reducing fossil fuel’s share of global primary energy (currently ~80%). Hence why I also get super excited about other hardware innovations, e.g., new manufacturing processes.

In sum? No silver bullets in climate, although solar is as close as you’ll get.